Safran: Compounding at Altitude

Safran: Compounding at Altitude

Overview

Safran is a business whose economics become clearer the longer one studies it. At first glance, it sits in a cyclical industry exposed to air traffic, aircraft production rates and defence budgets. Look more closely, however, and a different picture emerges: a company positioned at the most valuable choke points in global aerospace, with products that are designed once, paid for over decades, and increasingly monetised through recurring, high‑margin services. This combination is precisely what has historically underpinned many of our strongest long-term investments.

Safran operates across civil aviation, defence and aerospace equipment, supplying aircraft engines, landing systems, braking systems, avionics, navigation equipment, optronics and military propulsion systems. Its customers range from Airbus and Boeing to global airlines, leasing companies and defence ministries across Europe and allied nations.

What links these end markets is not their cyclicality, but the critical nature and longevity of Safran’s products. Engines and flight-critical systems are not discretionary purchases. Once selected for an aircraft platform, they are typically supported, serviced and upgraded over operating lives that can extend for 30 years or more.

The Power of Aerospace Economics

This structure creates an industry with exceptionally high barriers to entry. Developing a modern aircraft engine requires billions in upfront investment, a decade or more of certification, deep regulatory engagement, and the ability to support customers globally over decades. Very few participants capable of doing this on a scale, and fewer still with proven track records. As a result, competition occurs at the point of platform selection; once an engine is chosen, displacement risk is minimal. The economic payoff, however, comes later.

Nowhere is this clearer than in Safran’s most important asset: its 50% ownership of CFM International, the joint venture with GE Aerospace. Through CFM, Safran has played a central role in two of the most successful engine programmes in history. The CFM56 powered multiple generations of Airbus A320 and Boeing 737 aircraft and became one of the most profitable industrial products ever built. Its successor, LEAP, was designed to meet stricter fuel efficiency, emissions and noise requirements, and now dominates the current narrowbody market.

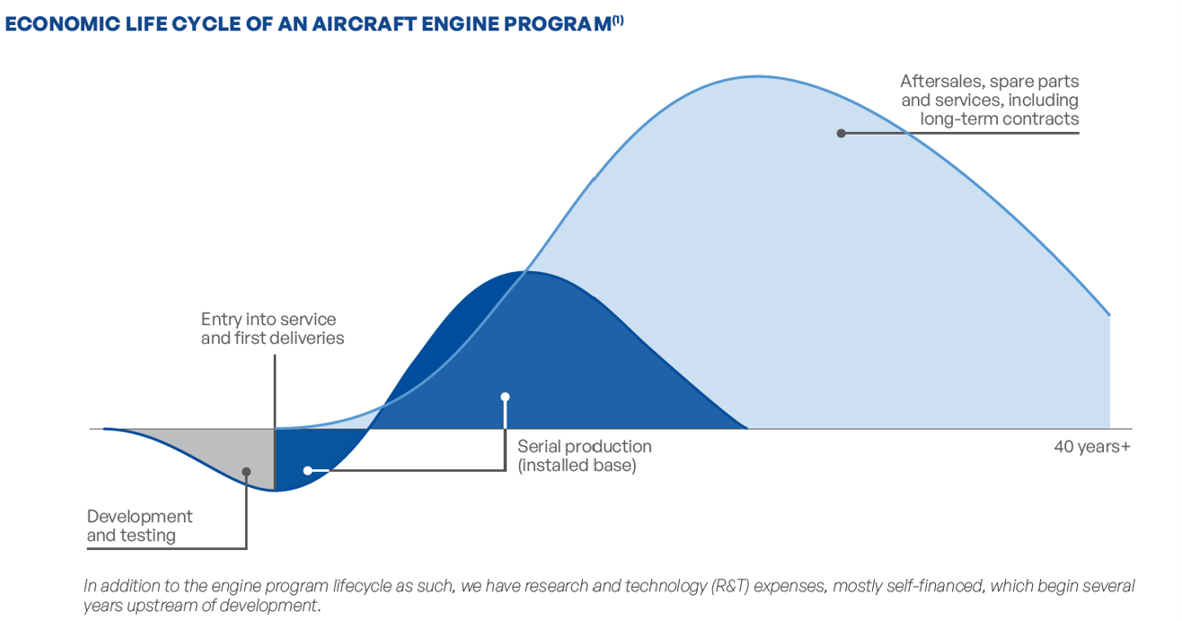

The transition from CFM56 to LEAP has been long and, at times, uncomfortable. LEAP required heavy upfront investment, introduced new manufacturing complexity through advanced materials, and initially diluted margins as fully amortised legacy engines were replaced with new units sold at low initial profitability. Supply-chain disruption during the post-pandemic ramp-up added further friction. For a period, returns on capital softened, masking the underlying strength of the franchise.

The Aftermarket Opportunity

That shift is now largely behind the company. LEAP production is scaling, unit costs are falling, and the installed base is still relatively young. This matters because commercial aerospace engines are typically sold close to breakeven, with most of their lifetime value earned later through spares, maintenance and overhauls.

As the LEAP engines mature and utilisation normalises, these higher-margin aftermarket revenues should become an increasingly important driver of profits. At the same time, growth is becoming less capital intensive, with incremental revenue now requiring less investment than it did five or ten years ago.

This is the core reason we expect returns on invested capital to rise meaningfully over time. Today, Safran’s ROIC sits in the low‑to‑mid‑teens, reflecting a business still digesting the effects of a major investment cycle. Over the next decade, as scale benefits accrue and the aftermarket expands, we see a credible path toward high‑teens returns, with the potential to approach 20%. Importantly, this improvement does not rely on heroic assumptions about demand, but rather on a favourable mix, greater maturity and steadily improving capital efficiency.

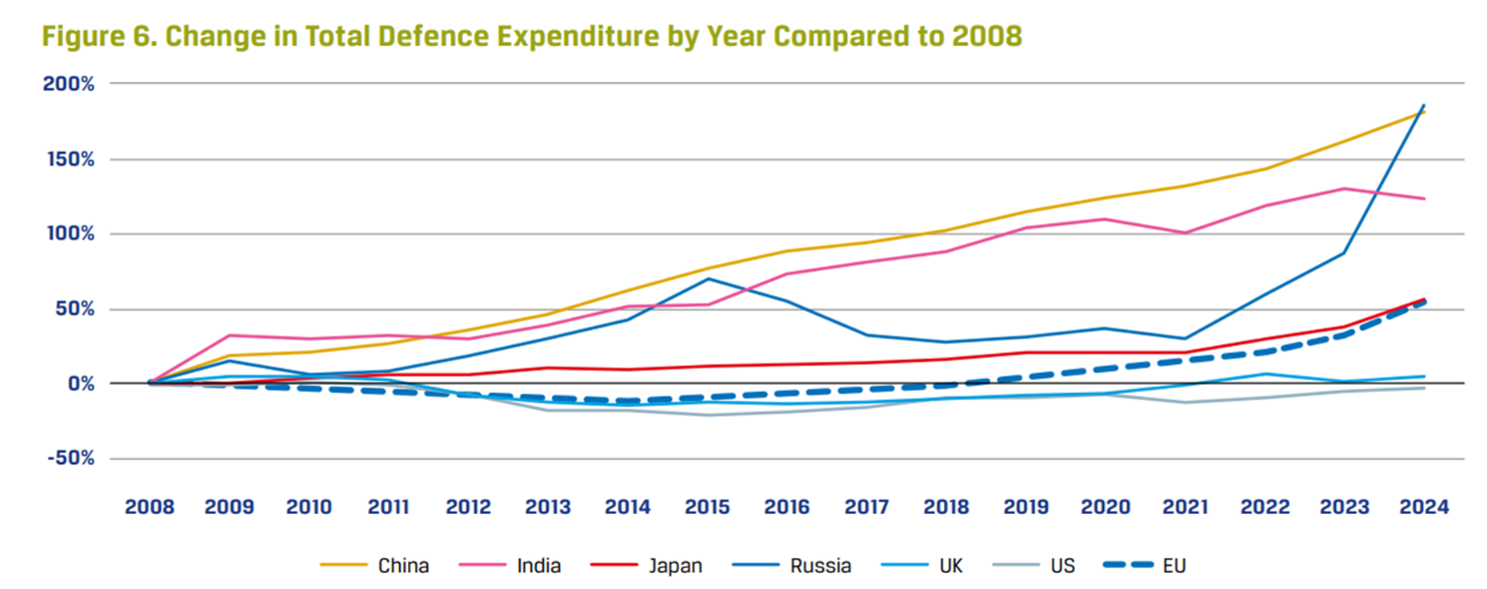

Alongside its civil aerospace business, Safran’s defence and aerospace activities provide a meaningful second engine of value creation. The company supplies military aircraft engines, navigation systems, optronics, guidance technologies and space equipment to defence ministries and government agencies. This segment is benefiting from a structural rise in defence spending across Europe and NATO, alongside heightened geopolitical uncertainty and a renewed emphasis on securing domestic and allied supply chains. Defence programmes are typically long-term, heavily regulated and technologically complex, which significantly limits the competitive landscape and supports more stable, predictable funding profiles.

While defence does not offer the same operating leverage as civil aftermarket activity, it adds resilience, visibility and attractive returns on capital. In portfolio terms, it dampens cyclicality and supports through‑cycle cash generation, thereby reinforcing Safran’s ability to continue investing and returning capital even during periods of softer civil demand.

Why We Continue to Hold

Taken together, these dynamics underpin our conviction that Safran can deliver above‑average revenue growth, alongside accelerating earnings and dividend growth. As operating leverage improves and capital intensity declines, free cash flow should grow faster than sales. With a strong balance sheet and disciplined capital allocation, this creates the conditions for sustained dividend growth over time — not as an explicit target, but as the natural outcome of improving industrial economics.

Safran is not without risks. Aerospace remains a cyclical industry, and execution is critical in complex manufacturing environments. But the company’s position at the most valuable points of the value chain, combined with a growing defence franchise and a maturing investment cycle, gives us confidence that it fits squarely within our framework for long‑term compounding: high revenue growth, rising returns on capital, strong free cash flow generation and durable dividend growth.

Disclaimer

Dundas Global Investors is the trading name of Dundas Partners LLP. Dundas Partners LLP is authorised and regulated by the Financial Conduct Authority (FCA) in the UK, the Securities and Exchange Commission (SEC) in the USA, and the Australian Securities and Investment Commission (ASIC) in Australia. The Authorised Corporate Director for the Heriot Investment Funds is Waystone Management (UK) Limited which is also authorised and regulated by the Financial Conduct Authority.

Dundas Partners LLP provides investment management services to clients in the UK, USA, Australia, and New Zealand. In this communication Dundas Partners LLP may be referred to as DGI, Dundas or Dundas Global Investors.

This document is a financial promotion and intended for professional, eligible counterparty and institutional investors only. The information presented is for the intended recipient(s) and is not to be shared or disseminated without our prior approval. This material has not been prepared for retail clients.

Investors are reminded that the price of shares and the income derived from them is not guaranteed and may go down as well as up. Past performance is not a reliable indicator of future results. This document contains information produced by Dundas and sourced from others where stated. The images used are for illustrative purposes only. The views expressed are those of Dundas and are based on current market conditions. They do not constitute investment advice or a recommendation to buy any security which has been highlighted in this material. Although this communication is based on sources of information that Dundas believes to be reliable, no guarantee is given as to its accuracy or completeness.

In relation to FCA handbook ESG 4.3, Dundas does not market these funds as a ‘sustainability product’. Use of any sustainability related terms in describing the characteristics of the strategy, or inclusion of any third-party information which measures sustainability of our portfolios are for information purposes only.

The MSCI® information contained herein: (1) is provided ‘‘as is,’’ (2) is proprietary to MSCI and/or its content providers, (3) may not be used to create any financial instruments or products or any indexes and (4) may not be copied or distributed without MSCI’s express written consent. MSCI disclaims all warranties with respect to the information. Neither MSCI nor its content providers are responsible for any damages or losses arising from any use of this information.

For full information on fund risks and costs and charges, please refer to the Key Investor Information Documents, Annual & Interim Reports, and the Prospectus, which are available on our website (https://www.dundasglobal.com). Recent performance information is also shown on factsheets, available on the website.