Powering the New Electric Age: Siemens Energy and the Infrastructure Supercycle

Powering the New Electric Age: Siemens Energy and the Infrastructure Supercycle

Overview

The global economy is entering a new electric age, but the constraint is no longer ambition, it is infrastructure. Behind every solar park, data centre and industrial park sits a less glamorous but essential layer of infrastructure that few companies in the world can meaningfully manufacture at scale: turbines, transformers, switchgear, substations, compressors and grid connections. Siemens Energy is one of them.

With leading positions across gas turbines, grid equipment, industrial energy systems and wind power, Siemens Energy touches nearly every part of the power value chain, from generation to transmission, from reliability to decarbonisation, and from large-scale industrial customers to the rapidly expanding electricity needs of data centres.

The company’s journey as a listed business has not been smooth. Historical financials were messy, and the troubled wind subsidiary, Siemens Gamesa, weighed heavily on profitability. However, the investment case today is increasingly defined by the scarcity value of mission-critical global supply, and a sharp rise in demand for electricity equipment after decades of underinvestment.

Siemens Energy is now expanding capacity into what increasingly looks like a multi-decade industrial buildout. Our internal work describes the position well: “the past is not prologue – it is much better.”

The Catalyst for Growth

The long-held assumption that power demand in developed markets would remain subdued has been overturned by three powerful forces: electrification, grid modernisation and the rapid expansion of data centres. Now, the global power system is being forced to expand at a pace it was never designed for.

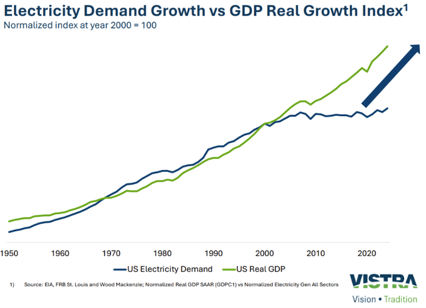

This chart from U.S. electric utility Vistra shows that since China’s ascension to the WTO, U.S. electricity demand and real GDP has decoupled. We believe this gap will start to close due to reshoring of industrial activities, data centre buildout and oil and gas electrification.

This shift matters because the bottlenecks are no longer onlyin software, permitting or capital. They are increasingly in physical equipment. Gas turbines, transformers and high-voltage grid components are complex, customised, safety-critical products with long lead times and limited global manufacturing capacity.

The gas turbine industry is effectively dominated by threemajor players: GE Vernova, Mitsubishi Heavy and Siemens Energy. That concentration gives suppliers meaningful pricing power and supports strongermargins. Similar dynamics are visible in grid equipment. Customers need toexpand transmission capacity, connect renewable generation, strengthen gridstability and support rising loads from data centres.

This is what makes this catalyst so compelling. The energy transition is not simply a one-year recovery story.It is the result of cumulative under investment meeting a structural acceleration in demand.

The Secret to Enduring Growth: Scarcity, Scale and Service

Siemens Energy occupies a critical position within the global power system. The number of credible suppliers is limited, technical barriers are high and customers increasingly prioritise reliability over lowest upfront cost.

The gas turbine business is a good example. New turbine orders can be lumpy, but the long-term attraction lies in the installed base and aftermarket opportunity. Once turbines are installed, they require service, maintenance, upgrades and parts over many years.

Grid Technologies offers a different but equally compelling growth engine. The business benefits from rising demand for transmission equipment, grid resilience and electrification infrastructure and is extremely difficult to displace due to decades of experience working with electric utilities, network operators and distributors of equipment.

The common thread across these businesses is scarcity value. These are not markets where capacity can be added overnight or where low-cost entrants can easily replicate capability. Products are technically demanding, customers are conservative, and failure can be extremely costly. In that context, reputation, installed base, engineering depth and execution reliability valuable competitive assets.

Financial Highlights and Diversification

Their financial recovery has been striking. Only a few years ago, the company was grappling with severe cash flow pressures and required government-backed guarantees to stabilise the business. Today, it is emerging as one of the world’s most strategically important suppliers of critical energy infrastructure.

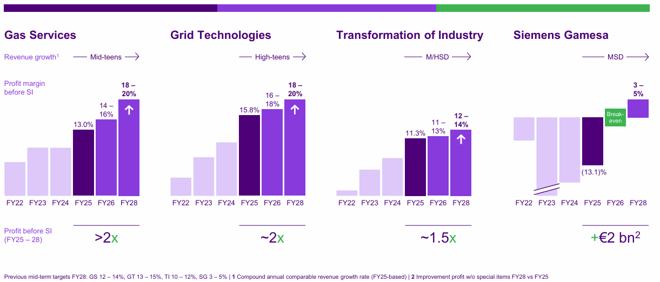

In FY2025, Siemens Energy reported orders of €58.9 billion, up 19.4% on a comparable basis, and revenue of €39.1 billion, up 15.2% on a comparable basis, with all major business segments contributing to growth. Profit before special items rose to €2.355 billion, compared with €345 million in FY2024, with improvement across the group.

Momentum continued into Q1 FY2026. Christian Bruch, CEO of Siemens Energy described the quarter as a “very strong start to the financial year”, with orders reaching a new record level, significantly improved revenue and cash flow, and earnings more than doubling compared with the previous year.

"We have made a very strong start to the financial year. Sustained high demand in our gas turbines and grid technologies businesses is making a significant contribution to overall performance. Also in the wind business, there are early signs of a modest improvement.”

The group’s order book provides meaningful visibility. At the end of FY2025, the order backlog reached a new record high of €138 billion, representing strategic scarcity value rather than simply future revenue. Siemens Gamesa, the wind farm business, remains the weakest part of the business, but it is showing early signs of improvement. Through our engagement with Siemens Energy, we believe that this business can be turned around through pricing and operational action, mirroring the structure we already see in the gas turbines market. Siemens Energy continues to target break-even at Gamesa by FY2026, setting the stage for a potentially powerful recovery.

Capital allocation is also becoming more attractive and aligned with a coherent long-term strategy. The company has guided to €6 billion of capex over 2026–2028, increasing manufacturing capacity by 30–50%, with capex peaking at around 5% of sales before normalising to around 3% after 2028 and settling below annual depreciation. Their annual R&D budget exceeds 3% of sales, or $1.3bn, and is focused on key customer requirements for greater efficiency, ease of use and installation and dual use of green fuels such as hydrogen.

The balance sheet recovery is also allowing Siemens Energy to return significant capital to shareholders. During the Gamesa situation and government guarantee negotiations, dividend payments were constrained. Those issues are now largely behind the company. Siemens Energy has reinstated its 40–60% dividend payout policy and plans approximately €10 billion of shareholder returns through dividends and buybacks over the coming years.

Why We Still Hold – Scarcity Value and Long-Term Tailwinds

Siemens Energy today is fundamentally different from the business the market feared during the height of the Siemens Gamesa problems. The balance sheet has been restructured, profitability has improved, cash generation has strengthened, and the core businesses of Gas Services and Grid Technologies have moved from recovery to expansion.

More importantly, the company now sits at the convergence of several of the most important investment themes of the next decade: electrification, grid modernisation, power security, industrial decarbonisation and AI-related data-centre demand.

There are still risks. Siemens Gamesa remains operationally challenging and a source of execution uncertainty. Nevertheless, this is precisely the kind of business where the market can often underestimate both the durability of a cycle when the starting point is decades of underinvestment and profitability is still in the early innings of a structural improvement.

In our view, Siemens Energy is no longer simply a recovery story. It is becoming a scarcity story: one of a small number of global suppliers positioned at the heart of the infrastructure build-out required for the next phase of electrification.

If the last decade belonged to digital platforms, the next may well belong to the companies that power them.

Disclaimer

Dundas Global Investors is the trading name of Dundas Partners LLP. Dundas Partners LLP is authorised and regulated by the Financial Conduct Authority (FCA) in the UK, the Securities and Exchange Commission (SEC) in the USA, and the Australian Securities and Investment Commission (ASIC) in Australia. The Authorised Corporate Director for the Heriot Investment Funds is Waystone Management (UK) Limited which is also authorised and regulated by the Financial Conduct Authority.

Dundas Partners LLP provides investment management services to clients in the UK, USA, Australia, and New Zealand. In this communication Dundas Partners LLP may be referred to as DGI, Dundas or Dundas Global Investors.

This document is a financial promotion and intended for professional, eligible counterparty and institutional investors only. The information presented is for the intended recipient(s) and is not to be shared or disseminated without our prior approval. This material has not been prepared for retail clients.

Investors are reminded that the price of shares and the income derived from them is not guaranteed and may go down as well as up. Past performance is not a reliable indicator of future results. This document contains information produced by Dundas and sourced from others where stated. The images used are for illustrative purposes only. The views expressed are those of Dundas and are based on current market conditions. They do not constitute investment advice or a recommendation to buy any security which has been highlighted in this material. Although this communication is based on sources of information that Dundas believes to be reliable, no guarantee is given as to its accuracy or completeness.

In relation to FCA handbook ESG 4.3, Dundas does not market these funds as a ‘sustainability product’. Use of any sustainability related terms in describing the characteristics of the strategy, or inclusion of any third-party information which measures sustainability of our portfolios are for information purposes only.

The MSCI® information contained herein: (1) is provided ‘‘as is,’’ (2) is proprietary to MSCI and/or its content providers, (3) may not be used to create any financial instruments or products or any indexes and (4) may not be copied or distributed without MSCI’s express written consent. MSCI disclaims all warranties with respect to the information. Neither MSCI nor its content providers are responsible for any damages or losses arising from any use of this information.

For full information on fund risks and costs and charges, please refer to the Key Investor Information Documents, Annual & Interim Reports, and the Prospectus, which are available on our website (https://www.dundasglobal.com). Recent performance information is also shown on factsheets, available on the website.